Construction costs have risen dramatically in recent years, making sustainable financing more important than ever for developers and business owners. Fortunately, construction managers have access to construction loans, a unique form of short-term financing designed to help you secure capital at each stage of construction. Here’s how to use one of these loans to manage cash flow and cover unexpected costs.

What you need to know

- Construction loans are drawn in installments at the end of each phase of construction, helping you manage cash flow and reducing the financial risk of large projects.

- These loans are unsecured and so have stricter requirements. Prepare your credit report, a down payment, a property appraisal, and a project plan before applying.

- Plan your project in full ahead of time, and mitigate risk by allocating extra budget for setbacks and managing your draws and payments with an accountant or bookkeeper.

What is a construction loan?

Construction loans are a unique form of unsecured short-term financing available to construction companies. They combine elements of term loans and lines of credit to better support you as you build and financially plan for commercial or real-estate building or renovation projects.

When you’re approved for a construction loan, you’ll be approved for a lump sum of funds that gets issued in installments, usually when each phase of construction is completed, and you pay interest only on what’s been drawn so far. This phased financing helps mitigate the risk of unforeseen obstacles in large construction projects.

You can take out multiple short-term construction loans to cover long-term projects, and some loans for residential projects can automatically convert into a traditional mortgage once the project is complete.

What are the benefits of construction loans?

The main benefit of construction loans compared to traditional term loans is their phased payout. Receiving your sum in installments—and only paying interest on what you’ve drawn, like a business line of credit—helps balance your budget across the whole project.

Construction loan requirements

As the business owner, you’re financially accountable for planning project budgets and repaying debts, but you should work with accountants or bookkeepers to decide the appropriate size and terms of any loans you apply for. To do that, assess the financial health of your business and your ability to provide the following:

- Credit and financial reports demonstrating strong credit score and financial health.

- A 20–25% down payment based on the total loan amount.

- An appraisal report, written by a licensed appraiser, that describes what the land and property will be worth once the project is finished. Your lender will likely hire their own appraiser, too.

- A blue book, or a comprehensive plan for your project that details each phase of construction, expenses, and loan repayment.

How construction loan lenders manage risk

Construction loans are unsecured and yet require large sums of money, so lenders tend to have stricter requirements for applicants. They’ll closely assess your financial health and construction plan to determine your creditworthiness, so don’t approach a lender before your blue book is finished.

Your lender may also require more actively in the construction project than traditional banks and mortgage lenders—for example, some lenders want proof that a phase was completed before releasing additional funds. Be sure to check terms and conditions on loans before you sign.

How construction loans impact long-term project planning

Construction loans establish an ongoing stream of capital at the outset of your project, eliminating the possibility of cash flow issues from lack of funding. Relying too heavily on your loan carries its own risks, but these can be mitigated with proper long-term planning.

Start with a strong roadmap, as the longer a project takes, the more interest will accumulate on your draws. Use this roadmap in your blue book to help lock in favorable loan terms, and be open to renegotiating if market conditions, labor strikes, or regulatory changes majorly disrupt operations.

Successfully managing one loan will improve your business credit, which will help you get approved for construction loans for future projects and marketing efforts.

How to choose the right construction loan

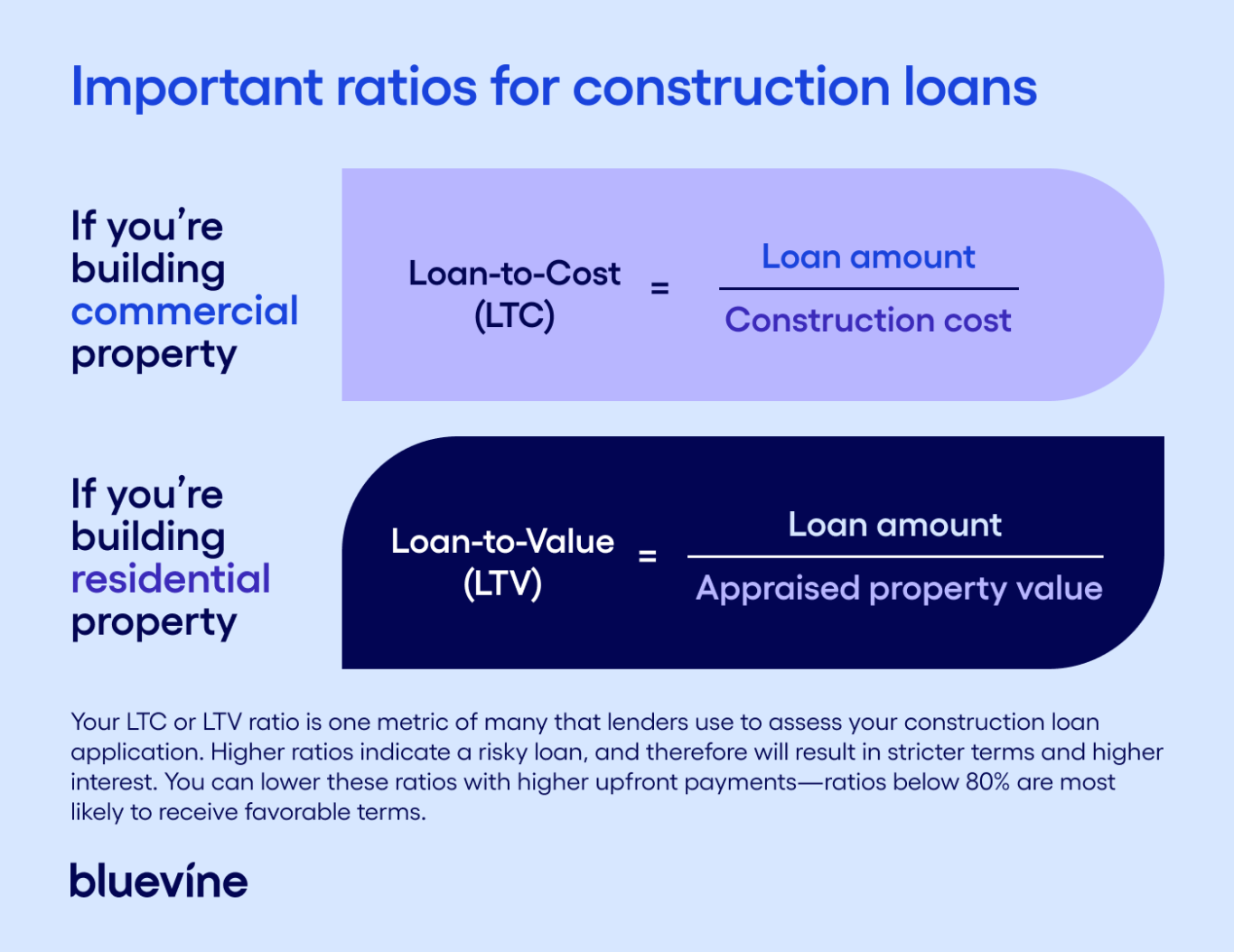

Construction loans tend to come from smaller institutions like regional banks and credit unions. Always choose an experienced lender and compare interest rates and loan terms based on your project’s scope and expected cost. You should also calculate your Loan-to-Cost (LTC) and Loan-to-Value (LTV) ratios, as these will affect your terms and payments:

3 common pitfalls and how to avoid them

Here are some common problems that can arise when using construction loans to support long-term projects:

1. Underestimating your budget and cash flow needs

If your loan is too small, you may experience cash flow problems and run out of funds between draws, which will impact your ability to pay subcontractors, complete your project, and repay the loan.

How to avoid

Work with your accountant or bookkeeper to analyze the cost of your construction project, then create a plan that aligns draws with project phases while allocating some extra budget for contingencies. Request itemized quotes from contractors.

2. Not planning for contingencies

Unexpected setbacks—like market changes, supply chain disruptions, labor shortages, or poor weather—can delay progress, extending your loan period and increasing interest payments.

How to avoid

When planning ahead, allocate 10–15% of your budget for unexpected delays or costs, and ensure you stay ahead of permits or compliance. Keep regular contact with subcontractors and plan for inflation. Stay updated on new laws, regulations, or codes in your area.

3. Taking on more debt than you can repay

Taking on too big of a loan will cause cash flow problems as you struggle to meet interest payments—and these can put your business in jeopardy when you encounter unexpected costs.

How to avoid

Work with your accountant or bookkeeper to only take on as much debt as you need—keep your LTC and LTV ratios beneath 80%. Lenders will probably reject your application if you lack the cash flow to repay the loan, but it’s best to ensure you can repay before applying.

Power your next project with a line of credit or term loan.